SITEMAP

HOT ISSUE

2026. 7

Korea’s economy remained on a modest recovery path, supported by robust semiconductor exports and services activity, while manufacturing production softened.

The More

SPOTLIGHT

LATEST REPORT

Structural Changes in Korea’s Retail Markets and Their Economic Impacts

Renewable Energy Deployment in Korea: Economic Drivers, Barriers, and Policy Implications

Macroeconomic Impact of AI Diffusion

Government Forms and Economic Security

Korean Real Estate Project Finance: Structure, Problems, and Policy Recommendations

Analysis of Commuting Efficiency based on Urban Spatial Development and Transport Infrastructure Supply Policies

A Study on the Economic Impact of Foreign Worker Inflows and Determinants of Migration Decisions

Intergenerational Mobilty in Korea: Insights from Educational Mobilty

Evaluating the Impact of Government Policy in the Pharmaceutical Sector: Analysis and Key Implications

Energy Market Design with Local Content Requirements

EVENT

Shifting the Economic Paradigm to Reignite Growth Conference with Nobel Laureate Peter Howitt

15 May 2026 (Fri), 13:10-17:40

Grand Ballroom, The Westin Josun Seoul National Research Council Korea, Korea Development Institute VIEW

MPB-KDI-IDB PIM Seminar Advancing Public Investment Efficiency

March 18 (Wed) - 20 (Fri), 2026

Fraser Place Central Seoul, Seoul, Korea MPB, KDI, IDB VIEW

Global Carbon Market Investment Forum

December 11, 2025(THU) ~ 12(FRI)

Global Knowledge Exchange and Development Center Ministry of Economy and Finance / KDI VIEW

2025 Knowledge Exchange Days

November 6, 2025(THU) ~ 7(FRI)

Global Knowledge Exchange and Development Center, Rose of Sharon Hall Ministry of Economy and Finance / Korea Development Institute VIEW

Ensuring Sustainable Infrastructure Delivery through Public-Private Partnerships 2025 Asia PPP Practitioners’ Network (APN) Conference

September23, 2025(TUE) ~ 25(THU)

Nine Tree Premier ROKAUS Hotel Seoul Yongsan, Seoul, Korea MOEF, KDI, WB, ADB, ADBI VIEW

AI for Economic Transformation 2025 KDI-World Bank Global forum

September 25(THU), 10:00 ~ 15:00 (KST)

Violet & Cosmos Hall(2F), The Westin Josun Seoul, Korea KDI, World Bank LIVE VIEW

The Role of AI in Fiscal Policy The 13th Korea-OECD International Forum on Budgeting

September 26(Fri), 09:30 ~ 17:30 (KST)

Grand Ballroom (5F), JW Marrirott Hotel Seoul MOEF, KDI, OECD VIEW

2025 G20 Global Financial Stability Conference Conference

September 3(WED), 09:30~16:40

Grand Ballroom(LL), The Plaza Hotel Seoul MOEF, KDI VIEWPERIODICALS

The July issue reassesses humanitarian cooperation amid prolonged inter-Korean estrangement and examines North Korea’s defense industry and related research. The special interview reviews KSM’s 30-year record and the rationale for revising its public name. It also discusses living conditions, market controls, regional development policy in North Korea, prospects for renewed humanitarian cooperation, and civil society’s role in peaceful coexistence. “Trends and Analysis” estimates defense-industry capacity utilization using power-sector conditions as a proxy and offers a long-term outlook. A second article assesses prospects for renewed growth, focusing on expanded weapons production, export opportunities from closer North Korea?Russia ties, and the parallel development of nuclear and conventional capabilities. “Economic Data” presents ten 2025 doctoral dissertations on the North Korean economy, organized by subject.

In many respects, 2025 can be understood as a year of transition for the North Korean economy. Rather than marking a decisive break from previous trends, the year reflected the authorities’ efforts to stabilize the gains achieved during the recovery period while simultaneously preparing the foundation for a new stage of economic development beyond the current Five-Year Plan. Although signs of improvement became increasingly visible in selected sectors of the official economy, important questions remain regarding the sustainability, scope, and structural implications of this recovery.

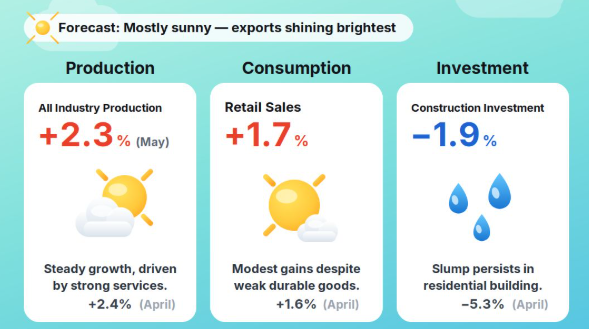

In May, total industrial production decreased, while retail sales increased. In June, the growth in the number of employed persons rebounded, and consumer price growth accelerated from the previous month. In May, the total industrial production fell (down 3.0% m-o-m and up 2.3% y-o-y) as a decline in industrial output (down 3.0% m-o-m and down 0.9% y-o-y) more than offset increases in services output (up 1.3% m-o-m and up 4.9% y-o-y) and construction output (up 3.8% m-o-m and down 1.9% y-o-y). Facilities investment moved down (down 0.1% m-o-m and up 9.7% y-o-y) and retail sales moved up (up 0.1% m-o-m and up 1.7% y-o-y). The cyclical indicator of the coincident composite index for May fell by 0.3 points and the cyclical indicator of the leading composite index increased by 0.7 points. In May, facilities investment moved down (down 0.1% m-o-m and up 9.7% y-o-y) and retail sales moved up (up 0.1% and up 1.7%). In June, the consumer sentiment index (CSI) went up by 0.5 points month-on-month to 106.6. The composite business sentiment index (CBSI) went down by 1.2 points to 97.7 and the CBSI outlook for July dropped by 2.4 points to 95.2. In June, exports climbed by 70.9 percent year-on-year, supported by expanded exports of semiconductor, computers, and ships. Average daily exports rose by 59.5 percent in June compared to the same month of last year. In June, the number of employed persons grew by 63,000 from a year earlier, and the unemployment rate remained unchanged at 2.8 percent. In June, the year-on-year consumer price index (CPI) climbed by 3.2 percent, up from 3.1 percent last month, while the index excluding food and energy rose by 2.5 percent, the index excluding agricultural products and petroleum products rose by 2.4 percent, and the CPI for living necessities increased by 3.4 percent. In June, stock prices remained flat, Korean Treasury Bond yields increased, and the Korean won weakened against the U.S. dollar. In June, both housing prices (up 0.33% m-o-m) and Jeonse (lump-sum deposits with no monthly payments) prices (up 0.38% m-o-m) continued to climb. The Korean economy has recently seen its recovery gain a firmer footing, following a marked acceleration in growth in the first quarter. Exports continued to increase sharply and domestic demand, including consumption, improved after temporarily losing momentum due in part to the impact of the war in the Middle East. However, cost-of-living pressures persist, including higher inflation and slower employment growth in the wake of the conflict in the Middle East. Although the global economy continues to grow at a moderate pace, the impact of the Middle East conflict has pushed up inflation in major economies and raised concerns over slower growth, while uncertainty surrounding international financial markets and energy prices remains. The government plans to make every effort to minimize the impact of the Middle East conflict by ensuring stable supplies of key goods and maintaining price stability. At the same time, it will swiftly implement the Economic Growth Strategy for the Second Half of 2026 to address structural challenges, including a post-conflict strategy for the Middle East, a rebound in potential growth, and measures to address economic polarization.

The Effects of Increased Korea Treasury Bond Issuance on the Yield Curve / MEEROO KIM AND JONG SOO HONG This study examines the impact of the sharp increase in Korea Treasury Bond (KTB) issuance following the COVID-19 crisis and analyzes the effects of bond buybacks as a policy countermeasure. Using a dynamic Nelson-Siegel model with macroeconomic factors, we estimate the effects of changes in the bond supply on the yield curve. Empirical results show that a KRW 1 trillion increase in KTB issuance raises yields by approximately 2.5 to 2.9 basis points, with stronger effects observed in the post-COVID period and in medium- to long-term maturities with weaker demand. Conversely, emergency buybacks reduce yields by about 1.9 to 2.1 basis points, with similar maturity dependent dynamics. These findings highlight the importance of demand conditions in amplifying the interest rate effects of government bond supply shocks. CBDC and Bank Money Creation / SUNJOO HWANG This paper examines the impact of a retail type of Central Bank Digital Currency (CBDC) on bank lending. While concerns exist that CBDC could reduce bank lending by diverting deposits from commercial banks to the central bank, this paper argues that the relationship between CBDC and bank lending is more complex because real-life banks do not lend out of deposits but instead create deposits by making loans. By examining a model of “fountain pen money” creation, the paper shows that a bank's lending capacity is influenced by both cash deposits and an augmentation factor. While CBDC reduces the capacity for lending as some deposits shift to the central bank, the magnitude of this reduction depends on the size of the augmentation factor and may not lead to a significant decrease in bank lending. In economies where banks lend close to their deposit base, such as in South Korea, the reduction in lending due to CBDC is likely to be marginal. Furthermore, this paper explores the social welfare implications of the contractionary effect of CBDC, showing that if the money creation constraint is weakly binding, CBDC can improve social welfare by mitigating excessive lending. Conversely, if the money creation constraint is strongly binding, CBDC may reduce social welfare by exacerbating credit shortages. The Effects of Parental Competitive Pressure on Private Education Investment / SUNGMIN HAN AND SEUNGJOO HAN In South Korea, education serves as a critical engine for social mobility, where academic credentials from prestigious universities function as a decisive factor in shaping career trajectories and earning potential. This dynamic has fostered intense educational fervor and led to the proliferation of a massive private education market. This study empirically examines the relationship between parental competitive pressure ? defined as a synthesis of achievement expectations and anxiety ? and investment in private education within a highly competitive educational environment. The analysis shows that private education expenditures are positively associated with parental competitive pressure. Notably, this increase occurs primarily through greater spending rather than an increase in total tutoring hours. This pattern suggests that, given children’s time constraints, highly pressured parents strategically prioritize quality over quantity. Furthermore, the effect varies across family backgrounds, indicating that reliance on private education reflects the interplay between socio-structural factors and household resources, thereby reproducing inter generational educational inequality. Overall, it was found that dependence on private education is a structural phenomenon amplified by status competition within a success-oriented society. Consequently, policy interventions should shift away from superficial regulations and focus on addressing the fundamental socioeconomic drivers of parental competitive pressure. Volatility Spillover Effects in Foreign Exchange Markets among China, Japan, and South Korea / BOK-KEUN YU AND KWON SIK KIM This paper analyzes the dynamic spillover effects of exchange rate volatility among the foreign exchange markets of China, Japan, and South Korea from January of 2010 to March of 2024 based on exchange rate determinataion theories, the GJR-GARCH model, and the TVP-VAR model. The key empirical results are as follows. First, while the factors determining the CNY/USD, JPY/USD, and KRW/USD exchange rates are somewhat different, it was found that CNY/USD is influenced by the short-term interest rate differential with the U.S., JPY/USD is affected by the VIX and by a COVID-19 dummy, and KRW/USD is impacted by the difference in the money supply change rate with the U.S. and the VIX. Second, the exchange rate volatility of the three currencies was found to exhibit the well-known persistence and leverage effects. Third, regarding the time-varying spillover effects of exchange rate volatility between the three countries’ foreign exchange markets, the transmission effects of exchange rate volatility between the three countries varied with the timing, frequency, and persistence.

| ■ | The Korean economy showed signs of a broader improvement,led by semiconductor-related sectors. | |

| ○ | Exports and equipment investment continued to grow strongly, driven by semiconductors, while consumption growth accelerated, led by durable goods. | |

| ○ | All-industry production posted relatively high growth, as services maintained a favorable trend and manufacturing rebounded. | |

| - | Services production continued to grow at a strong pace, led by financial and insurance activities and professional, scientific, and technical services. Manufacturing production also rebounded across most industries, including motor vehicles and machinery and equipment. | |

| ○ | However, uncertainties persist both at home and abroad amid ongoing U.S. tariff measures, instability in the Middle East, still-elevated inflation, and weakening employment conditions. | |

SNS

TOP VIDEO PICKS

Recommend VOD

Popular VOD

The Structural Risks Behind Korea’s Exposure to U.S. Tariffs

Rising Health Insurance Expenditures: Premium Hikes Aren’t Enough

Toward a 20% Equity Ratio in Real Estate PF

The Economics Behind The Rise of K-Content

#Corporate Studies: Business Strategy #Industry Studies : Service Business #Market StructureKorea Development Institute

NEWS

-

KDI News

Vietnamese Delegation from CPV Central Commission

Jul 31, 2026 -

KDI News

「2026 International Conference on Economic Education: Reconstructing Economic Education in the AGI Era」 Held

Jul 29, 2026 -

KDI News

ADB CAREC CSPPF-KDI GKEDC 「Korea Outreach and Business Engagement Seminar」

Jul 20, 2026 -

KDI News

KDI GKEDC hosts 「K-POP as a Global Cultural Industry」

Jul 20, 2026 -

KDI News

「The Future of Work: A New Labor Market in Coexistence with AI」 Policy Forum Held

Jul 20, 2026

World's Leading Think Tank, Korea Development Institute.